Tax pundits have been telling us for many years that income tax on dividends would increase. That moment finally arrived in the Summer Budget 2015 but we never thought it would be like this.

Our beloved imputation system – designed to prevent double taxation of corporate profits – will be consigned to the fiscal dustbin on 6 April 2016. The Treasury points out that this regime was “designed more than 40 years ago when corporation tax was 50 per cent and the total bill on dividends for some was over 80 per cent”. Similarly, the (non-reclaimable) 10% tax credit that has been carried with dividends since April 1999 will be scrapped.

In its place, Chancellor George Osborne unveiled a progressive series of dividend tax rates that will ‘kick-in’ from 2016/17. However, dividend income will benefit from a new £5,000 tax-free allowance. Taxable dividend income in 2016/17 will be taxed at the special tax rates shown in the table below

| Dividend tax rates – 2016/17 | ||

| Taxable dividend income* | Tax rate** | Comparable rate in 2015/16 |

| Up to £32,000 | 7.5% | Nil |

| Between £32,000 and £150,000 | 32.5% | 25.0% |

| Above £150,000 | 38.1% | 30.6% |

| * Total dividend income after £5,000 exemption and any available personal allowance | ||

| ** Rate applies to actual dividend received with no grossing-up | ||

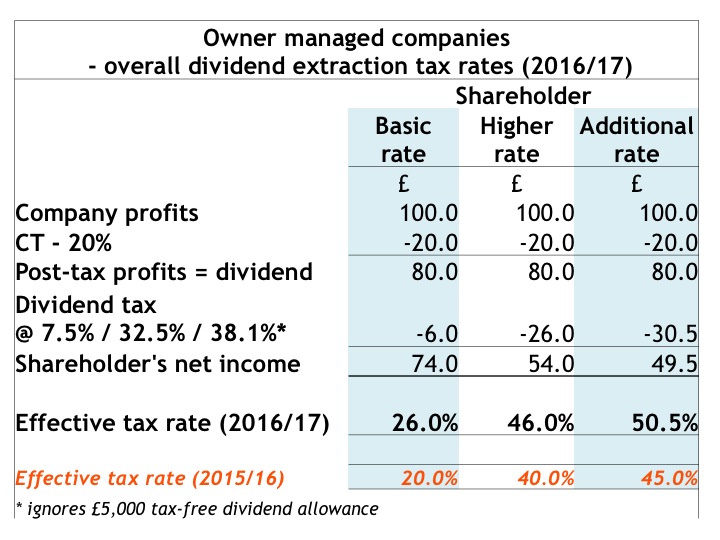

From 2016/17, the new dividend tax regime brings in much higher tax rates. A review of the total tax costs (including corporation tax) of paying dividends out of a typical owner-managed company is provided below:

Owner-managers will look at this table with some dismay – these are significant increases. For many years now, most owner managers have pursued a ‘low salary/high dividend’ profit extraction model since this proved to be more tax efficient. Dividends were taxed at lower rates than earnings and they did not attract (Class 1) national insurance contributions (NICs).

Companies that exploit the ability to pay ‘tax-free’ dividends of around £35,000 to spouses will now see such amounts taxed at 7.5% from 2016/17. This should still produce typical tax savings of 25% (i.e. 32.5% less 7.5%) of the dividend and hence such planning will still be worthwhile.

The 2016/17 increases in dividend tax will narrow the tax differential between bonuses and dividends, so that dividends become only marginally preferred – see example of ‘bonus v dividend’ comparison below:

Many owner managers are likely to consider accelerating dividend payments before April 2016 to benefit from the current lower rates. Provided ‘their’ companies have sufficient distributable profits, additional dividends can be paid out. If the company still needs the cash for working capital or future investment, it can be ‘invested’ back in the company as a director’s loan. Bringing forward dividends to the current tax year means advancing the tax due on the dividend but this disadvantage will be outweighed by the tax savings.

Some owner managers will now seek to retain more profits within the company at low rates of corporation tax (which should reduce to 18% by 2020). There may also be a tendency to take out these reserves on ‘retirement’ via a ‘capital’ company purchase of own shares transaction.

It appears, HMRC has no plans to increase the 25% ‘section 455’ tax charge on loans to participators. This is bound to encourage more owner managers to ‘live’ off overdrawn loan accounts at a reasonably palatable tax rates (especially with the beneficial loan charge currently based on an interest rate of 3.25%).

The hike in dividend tax rates is expected to swell the Treasury’s coffers by some £2 billion a year and is one of the biggest revenue raisers in the Summer Budget. However, the Treasury may have underestimated the behavioral response of owner managers and the predicted tax take may well fall short of that figure – due to the ‘laffer-curve’ effect, but that is a discussion for another day.

Peter Rayney